COVID-19 became an unexpected equalizer. It respects no one. It discriminates against no one. Walang arti-artista, walang pulitiko. Lahat pwedeng tamaan nito. Wala siyang sinasanto. This virus has revealed the true colors of our world. Sino ba ang essential sa lipunan? Sino ba ang mapagbigay? Sino ang may compassion? Anu-ano pa ang dapat nating gawin to be better?

This Enhanced Community Quarantine gave me so much time to reflect on life. And here are my personal takeaways.

LIFE

Noong wala pa itong virus, sobrang busy nating lahat para magtrabaho. Marami tayong gustong maabot. Promotion, financial empire, malalaking bahay, mabibilis na kotse, travel around the world. Ngayon na limited na ang ating activities at may threat ng isang disease, maiisip mo na lang na may mas mahahalaga pa pala kaysa sa mga materyal nating mga pangarap. Yung mga dating akala mo ay essential sa buhay, mare-realize mo na lang na kaya mo palang mabuhay kahit wala ang mga iyon.

At dahil rin sa ECQ, natutunan ko na kapag mawala ang lahat ng mga pangarap at mga pinagtrabahuhan natin, ang matitira lang ay ang ating pamilya at ang Diyos. Kaya sana ngayong ECQ, let’s spend more time with our family and with God. Gamitin natin ang oras natin to know them more and to love them more. Dahil sa huli, our relationships are the only ones that matter most.

FAITH

Dahil nga busy tayo sa trabaho, madalas nating nakalilimutan ang ating spiritual life. Masyado tayong nakatuon sa physical life natin at nakalilimutan na nating pasiglahin ang ating kaluluwa. Pero dahil sa virus na ito, ang mga dating nakalilimot manalangin ay bumabalik na sa Diyos. Ang mga busy para mag-pause man lang para kausapin ang Panginoon ay natututo nang manalangin.

Nakita nating lahat na kahit sino pwedeng tamaan ng virus. Dahil dito, na-realize natin na we do not really control our lives dahil maaaring sa isang sakit, bigla na lang itong mawala. COVID-19 is a very good time to humble ourselves to our Creator. He gives and takes away. He made us and He knows kung hanggang kailan lang tayo sa mundo. Kaya better na bumalik tayo sa Panginoon at kilalanin natin muli Siya as our personal Lord and Savior.

FINANCES

No one hoped for this illness to invade the world. But there is always no harm in preparing for the worst. Kaya being financially prepared can really help us especially during a crisis.

Napansin mo ba na nare-reveal kung sino ang financially prepared at kung sino ang hindi sa panahong ito? Those who have savings, nakapag-impok sila ng food supplies that can last months. May peace of mind sila while ECQ. Pero those na walang savings, wala silang purchasing power to stock up. Habang ang iba ay nagpa-panic buying, maaaring ikaw ay nagpa-panic lang dahil wala kang pang-buy. Those who are not financially secure ay napipilitang maghintay sa ayuda galing sa gobyerno.

I hope that after this ECQ, mag-iba na ang ating pagtingin sa pera. Nawa mas maging masinop na tayo para magkaroon na tayo ng emergency fund. You will have peace of mind because you know you have savings that will protect your family against this crisis.

“Ngayon natin makikita ang halaga ng pag-iimpok dahil hindi naman natin makikita kung kailan ang mga ganitong emergency.” -Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Anu-ano ang life lessons na nakuha mo sa krisis na ito?

Anu-ano ang mga improvements na gagawin mo after ECQ?

Paano mo mapahahalagahan ang iyong pamilya at ang iyong spiritual life?

—————————————

WATCH THIS VIDEO:

Life Realizations with Jodi Sta. Maria

https://youtu.be/tYCwK2fQZOM

ARE YOU SICK AND TIRED OF YOUR PERSONAL, PROFESSIONAL AND FINANCIAL LIFE?

If you are, BEST NEWS! Your worry days are over!

Two of the best speakers in the Philippines come together for a special FB live course. Join me and my mentor, Francis Kong, on APRIL 18 SAT, 9PM Entitled: “YOUR BEST FINANCIAL YEAR EVER”

Click here to register and avail the EARLY BIRD RATE of Php 598 instead of Php 2,598: https://chinkeetan.com/best

For more inspirational content, new products, and promos, follow my Social Media accounts:

Ang daming ganap sa buhay natin ngayon. Lahat tayo ay apektado dahil sa pandemic na ito. Buong mundo ang sinubok ng matinding sakit na ito.

Pero sa kabila ng mga ito, ano nga ba ang naidudulot ng kaganapan na ito?

IT MADE US STRONGER

“Hindi ko na ata kaya.”

“Wala nang pag-asa ito.”

“Mamamatay na ata kami.”

Ilan lamang ito sa mga maririnig natin sa ibang mga tao. Kaya naman, mahalagang siguraduhin nating malakas ang ating isipan at loob. Hindi lamang labanan ng pisikal ang usapan dito.

Kaliwa’t kanan din ay sinusubok ang ating mental at emosyonal na lakas. Kaya iparamdam natin kahit sa simpleng pakikinig na tayo ay magkakaramay na lumalaban para maka-survive sa panahong ito.

IT MADE US WISER

“Pagkatapos nito, sisimulan ko na ang emergency fund.”

“Aalisin ko na ang mga bisyo ko. Mag-iipon na lang ako.”

“Babawasan ko na ang mga malalaking gastusin na hindi naman kailangan. Uunahin ko na ang needs.”

Ang mga pagsubok ay nagiging daan upang mas matuto tayo at mas magkakaroon tayo ng malinaw na direksyon sa kung ano ang mahalagang gawin habang tayo ay nabubuhay.

IT MADE US CLOSER

Nagiging malapit din tayo sa mga taong mahal natin at mga taong maaaring hindi natin napahahalagahan, ngayon ay mas nabibigyan natin ng halaga ang kanilang ginagawa para sa atin.

Mas napalalapit din tayo sa ating Panginoon. Alam natin na sa kabila ng mga pagsubok na ating nararanasan, hindi Niya tayo pinapabayaan. Kaya naman, huwag lang tayo mag-focus sa mga problema…

“Look at the bright side. Try to look at positive things and find solutions.” – Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Anu-ano ang mga babaguhin mo sa buhay mo simula ngayon?

Paano mo pag-iipunan ang iyong emergency fund?

Gaano kalakas ang iyong paniniwala sa pagmamahal ng Panginoon?

——————————————-

Watch this video:

ANO ANG GAGAWIN MO KAPAG IKAW AY GULONG-GULO!

For more inspirational content, new products, and promos, follow my Social Media accounts:

Nababalisa na dahil pare-pareho na lang ang nakikita mo sa inyong bahay?

Iritable na dahil feeling mo nakakulong ka sa inyong tahanan?

Nawawalan na ng pag-asa dahil hindi mo alam kung hanggang kailan itong krisis?

Kung ganito ang nararamdaman mo, maaaring ikaw ay nakararanas ng cabin fever. This is our body’s reaction towards isolation or being in a place for a long period of time. Ngayon na na-extend ng dalawang linggo ang ating Enhanced Community Quarantine (ECQ), kumusta ka? Kumakapit ka pa ba? Here are some simple ways to overcome cabin fever.

GET UP AND MEDITATE

Alam mo ba kung bakit umpisa pa lang ng araw ay ang baba na agad ng energy mo? Dahil hinayaan mo ang sarili mo na magpagulong-gulong sa kama. Pagkamulat ng mata, hahawakan agad ang phone, at magugulat ka na lang na ilang oras ka nang nagso-scroll ng newsfeed. Nasa kama ka pa lang, hindi pa naka-ready ang isipan mo, na-absorb mo na agad ang lahat ng negativity mula sa social media.

Kaya bago mo pa i-check ang iyong FB, bumangon ka muna at mag-meditate or quiet time. You can pray, you can say what you are grateful for, you can read God’s Word. Feed your soul muna bago you dive into your newsfeed. Encourage yourself first thing in the morning bago ka sumabak sa mundo. If you do this, you would find yourself having a better outlook on life and with this crisis.

FIND A HOBBY

Kung dati ang default mode mo ay work, ngayon naman find time to have a hobby. It will break the monotony of your “as usual” quarantine day. Nakalulungkot talaga kung pare-pareho na lang ang nakikita mo at pare-pareho na lang ang ginagawa mo. So, find something that would excite you. Go online and learn something new. Ngayon na sumobra naman ang time natin on our hands, now is the right opportunity to pursue the thing that you have been putting off for the longest time.

FOLLOW A ROUTINE

Kahit na it is important that you find something that would break the monotony of your day, better pa rin that you give your day a structure. Make a routine and do your best to follow it. A routine is like a map or a guide on how you want your day to turn out. As you follow it, you will have a sense of organization and accomplishment, at ang importante ay you can have the feeling that your day has direction. Even if we are living in uncertain times, it is always better that we train our minds to seek direction. Direction points us to our purpose, and if we are living according to our purpose, kaya natin pagtagumpayan ang krisis na ito. Mayroon tayong rason para kumapit sa Panginoon at ipagpatuloy ang laban ng buhay.

“Mahalaga ang daily routine para mas maging productive at hindi ma-bored sa panahon ngayon.” Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Anong nararamdaman mo ngayong extended ang ECQ?

Ano ang itsura ng araw mo? Anu-ano ang ginagawa mo?

Paano mo nilalabanan ang boredom or cabin fever?

————————————–

WATCH THIS:

ANG TOTOONG MAY CONTROL NG MUNDO

For more inspirational content, new products, and promos, follow my Social Media accounts:

Halos one month na tayong naka-quarantine and we do not know when this will be all over. Kumusta ang pakiramdam mo? Nag-aalala sa buhay mo at para sa mga mahal mo sa buhay? Hindi ka ba makatulog?

Let me encourage you today with God’s Word from Proverbs 3:5-6,

“Trust in the Lord with all your heart and lean not on your understanding; in all your ways submit to Him, and He will make your paths straight.”

TRUST IN THE LORD

Mabigat ang salitang trust o pagtitiwala. Siguro ilang beses na tayong naka-encounter na nasira ang ating trust sa isang tao. Nasaktan tayo at nangako na magiging maingat na sa pagtitiwala sa iba.

Pero, ibahin natin ang Panginoon. If we really know God, we can trust Him because we know that He is a good Father. Ang mga ama dito sa lupa, they are not perfect. Maybe nasaktan nila tayo o hindi sila nakapag-provide nang sapat. Pero the Lord is our Heavenly Father. He is a perfect Father. He protects, He provides, and most of all, He loves. His love and mercy is all over His Word, lalo na when He sent Jesus to save us all from our sins.

Kaya sa panahon ngayon, let’s put our trust in the Lord. Magtiwala tayo na kahit hindi kagandahan ang nangyayari sa mundo natin ngayon, lahat ng ito ay may purpose. Hindi man natin maintindihan sa ngayon, pero our hearts can rest in the fact that the Lord is the Creator of everything and He holds the Universe. He knows what He is doing.

LEAN NOT ON YOUR UNDERSTANDING

Sabi sa Jeremiah 17:9, “The human heart is the most deceitful of all things, and desperately wicked. Who really knows how bad it is?”

Dahil deceitful o mapanlinlang ang puso, hindi dapat ito pagkatiwalaan. Naalala mo na isang episode pa lang ng Kdrama parang gusto mo na kaagad magka-jowa. Nakabasa ka lang ng isang post ng friend mo sa FB na taliwas sa paniniwala mo, parang gusto mo na kaagad makipag-away. Our emotions can get easily swayed.

Mabilis matakot ang puso. Mabilis masaktan. Kaya nga dapat huwag tayong mag-focus sa feelings o emosyon. Parating i-counter check sa isipan kung tama ba ang nararamdaman. Kaya nga nilagay ng Panginoon ang isipan na mas mataas kaysa sa puso so we can let our minds rule us and not our deceitful hearts.

GOD’S COMFORT

Obedience unleashes blessings. After ng instruction na pagkatiwalaan Siya and to surrender all to Him, God promises to make our paths straight. This can mean blessings in different forms. Maybe good finances, restoration of relationships, good health, o kung ano pa man. But I believe, if we put our trust and surrender everything to the Lord ngayong panahon na ito kahit full of uncertainties, He will protect us and higit sa lahat, He will comfort us.

Iyang takot at pangamba na nararamdaman mo ngayon dahil sa virus, that can go away if you would only learn to fully surrender your life to the Lord. That fear of what you will eat for the next days ngayong quarantine kahit na wala kang trabaho, surrender that to the Lord. He is the Ultimate Provider. That fear of what will happen next, surrender that to the Lord. He gives rest to the anxious heart.

Sa panahon ngayon na hindi mo alam ang susunod na mga kaganapan, there is one thing that you can do: Trust in the Lord with all your heart. And see how that will change your life and your perspective towards this crisis.

“Put your trust in Him. Lean on Him.” – Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Anong nararamdaman mo ngayong extended ang quarantine?

Paano mo nilalabanan ang takot at pangamba?

Ano ang panalangin mo sa Panginoon ngayong krisis?

————————————————————

WATCH THIS: SA PAGSUBOK: TRUST IN THE LORD https://youtu.be/8M47tR7siTM

For more inspirational content, new products, and promos, follow my Social Media accounts:

Marami sa atin ang natatakot ngayon dahil sa mga kaganapan sa ating bansa. Nandyan ang pagkakaroon ng takot na mawalan na ng makakain, mawalan ng trabaho, mawalan ng negosyo at marami pang iba.

Kaya naman ngayon, nais kong magtulungan tayo upang lahat ay sabay-sabay na makaahon. Nais kong tulungan n’yo rin ang iba kahit sa simpleng paraan.

SELF REFLECT

Unang-una sa lahat, alamin mo kung nasaan ka ngayon. Ikaw ba yung hirap na hirap sa sitwasyong ito? Ikaw ba yung nakakaluwag-luwag at may maibibigay sa iba o ikaw ba yung sapat lang ang naitabi para maka-survive sa panahong ito?

Mula dito, ano ang gusto mong baguhin at alisin para hindi na mauwi sa ganitong kalagayan. O kaya naman, ano naman ang gusto mong i-retain at i-sustain dahil ito yung nakikita mong tamang ginawa mo na dapat mo pang ipagpatuloy.

SET CLEAR FINANCIAL GOALS

“Dapat matutunan ko kung paano magsimula ng negosyo online.”

“Dapat may emergency fund ako para handa sa mga pagsubok.”

“Dapat alisin ko na ang mga hindi naman kailangan pagkagastusan lalo na ang mga bisyo at luho.”

Ganito na tayo dapat mag-isip. Huwag lang natin isipin ang problema sa puntong ito. Kailangan maghanap na tayo ng solusyon at magsilbing aral ito sa ating lahat.

SPEND MORE TIME WITH HIM

Nagkataon din na lenten season ngayon. Pagkakataon din para ipagdasal natin ang ating sarili at ang buong mundo para sa kaligtasan at proteksyon mula sa ating Panginoon.

Hinding-hindi Niya tayo iiwan at pababayaan. Mahal tayo ng Diyos kaya huwag nating ubusin ang lahat ng natititrang lakas at oras natin para lang sa takot at pangamba.

“Surrender all your fears to the Lord because the Lord loves you more than you love yourself.” – Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Ano ang financial goals mo ngayon?

Paano mo mas palalawigin ang iyong kaalaman para matutunan ang iba’t ibang bagay?

Gaano katibay ang iyong paniniwala at pagmamahal sa Panginoon?

Watch this video:

SPIRITUAL AND PRACTICAL ADVICE with Bo Sanchez

ARE YOU SICK AND TIRED OF YOUR PERSONAL, PROFESSIONAL AND FINANCIAL LIFE?

If you are, BEST NEWS! Your worry days are over!

Two of the best speakers in the Philippines come together for a special FB live course. Join me and my mentor, Francis Kong, on APRIL 18 SAT, 9PM Entitled: “YOUR BEST FINANCIAL YEAR EVER”

Click here to register and avail the EARLY BIRD RATE of Php 598 instead of Php 2,598: https://chinkeetan.com/best

For more inspirational content, new products, and promos, follow my Social Media accounts:

Do You Want to Have a Happier, Productive, And Financially Empowered Team?

Introducing the Chinkee Tan Money Management Program – the solution to your employees’ money challenges. Watch as your team becomes smart with finances, leading to better performance and business success!

Invite Chinkee Tan

Your team's mentor for lifelong financial freedom.

He’s not just a money expert; he’s an EDUTAINER. With a mix of knowledge and entertainment, Chinkee makes money management fun and relatable. His program can transform your team’s financial mindset, leading them to a happy & successful financial path.

Explore how money mindsets shape behaviors towards earning, spending, and saving.

Unlock the secrets to a positive money mindset that drives success.

TOPIC 2

Savings 101

Uncover the secret to saving more without increasing income.

Shift your perspective on savings for long-lasting results.

Grasp the ultimate savings formula for sustained financial growth.

TOPIC 3

Maximizing Your Wealth

Learn ways to generate extra income without leaving your current job.

Discover the strategies that the rich use to increase their assets.

TOPIC 4

Debt 101

Explore the different types of debt and how to avoid them.

Uncover the 4-step process to escape the cycle of debt.

Workshop on personalized strategies to get out of debt.

TOPIC 5

Budgeting 101

Understand the relationship between budgeting and savings.

Master the 3 D's of budgeting and learn to create successful budgets in just 60 days.

PLUS: Workshop on effective budget creation.

Explore financial management for singles and retirees.

Length of Program: 1 to 2 hours

TOPIC 6

Money & Relationships

Learn how family influences finances and discover strategies to manage money effectively.

Gain insights into budgeting and financial planning for couples.

Master the art of saying no to those who misuse your generosity.

Explore financial management for singles and retirees.

Length of Program: 1 to 2 hours

TOPIC 7

Investment 101

Understand the true essence of investment.

Navigate the 4 Stages of Building Wealth.

Discover how to double your money through smart investments.

TOPIC 8

Preparing for Retirement

Preparing the workforce to enjoy their golden years.

Tips and strategies to retire early even with limited income.

The best wealth growth strategies to help you retire.

And Many More!

Who Should Attend?

Employees who want to take control of their finances. If your team is looking to save, budget, stay or get out of debt, or learn how to invest, this program is the answer.

Length of Program: Whole Day

Benefits for Employers

Increased Productivity: Financially secure employees are more focused and productive.

Boosted Morale: Empower your employees to take control of their financial future, and watch their confidence and satisfaction soar.

Reduced Turnover: Invest in your employees' financial well-being, and they're more likely to stay loyal to your company.

Enhanced Reputation: Demonstrate your commitment to employee well-being and be recognized as an employer of choice.

Relieve your team from financial stress. Book Chinkee Tan today!

What You Get: Chinkee Tan’s captivating and motivational talks that inspire attendees to reach their financial goals.

Benefits: Your employees will gain invaluable insights into financial management, mindset shifts, and practical strategies to overcome financial challenges. They’ll walk away motivated and equipped with actionable steps towards financial success.

What You Get: Engaging workshops led by Chinkee Tan, offering hands-on learning experiences in all areas of personal finance.

Benefits: Equip your team with practical tools, resources, and strategies to better manage their finances. These workshops empower them to make informed decisions, create effective budgets, and plan for a financially secure future.

What You Get: One-on-one coaching sessions with Chinkee Tan, tailored to address individual financial concerns and goals.

Benefits: Your employees will receive personalized advice and action plans to conquer their financial hurdles. With Chinkee Tan’s expertise, they’ll develop customized financial roadmaps, accelerate debt reduction, and make informed investment decisions.

What You Get: Comprehensive online courses by Chinkee Tan, accessible at your employees’ convenience.

Benefits: Allow your team to learn at their own pace with detailed modules on budgeting, investing, debt management, and more. These courses will empower them to enhance their financial literacy and make sound financial choices.

What You Get: A wealth of books, guides, and resources from Chinkee Tan that simplify complex financial concepts.

Benefits: Provide your employees with valuable information on personal finance, money mindset, and wealth-building strategies. These resources serve as ongoing references for continuous learning and self-improvement.

What You Get: Engaging webinars and seminars led by Chinkee Tan that delve into the secrets of financial success.

Benefits: Your employees will gain a deeper understanding of key financial principles, learn actionable strategies, and have the opportunity to ask questions in real-time. These sessions create an interactive learning environment that fosters deeper comprehension.

What You Get: Tailored corporate training programs by Chinkee Tan, designed to address your organization’s specific needs.

Benefits: Boost your employees’ financial literacy, reduce financial stress, and enhance overall productivity. Corporate training cultivates a positive work environment by equipping your team with invaluable financial skills.

Chinkee Tan’s services offer a holistic approach to financial education and empowerment, catering to diverse learning preferences and requirements. Whether through inspiring talks, engaging workshops, or personalized coaching, empower your employees and your organization to embark on a journey towards financial success with confidence.

Chinkee Tan or “Mr. Chink Positive!” is a wealth coach and motivational speaker. He is a Radio and TV Personality and the host of “CHINK POSITIVE.

He is also the author of several bestselling books, including “Till Debt Do Us Part: Practical Steps to Financial Freedom,” “For Richer and For Poorer,” and “Rich God Poor God” to name a few. Two of which are the “Diary of A Pulubi” and “My Ipon Diary”.

Chinkee is a financial expert, whose passion in life is to help people experience financial freedom and help free them from debt. His mission is to see more Filipinos become wealthy and debt-free.

Chinkee Tan serves a vast clientele of companies and individuals through the programs and materials it produces and distributes. The main clientele would be Filipinos, but Chinkee Tan has also been known to impart learnings to other nationalities as well.

Chinkee Tan has served include organizations and departments in finance, consumer goods, real estate, investments, insurance, church and religious organizations, education, franchising, food and beverage, government and many others.

He has worked with both small enterprises and large corporations.

Day 18 na ng Enhanced Community Quarantine. Kumusta ka Ka-Chink? Kumakapit pa o may cabin fever na? Productive pa ba o nag-Tiktok na? Sa mga ganitong panahon na wala tayong pwedeng puntahan at buong araw lang tayong nasa bahay, gayahin natin si Earl. Early bird na, masipag pa. Maaga gumising para simulan ang araw at ginagamit sa tama ang oras para hindi maburo sa bahay. Ano ba ang ginagawa ni Earl?

BE FIT AND HEALTHY

Dahil hindi ka makalabas ng bahay, kain-tulog repeat na lang ang buhay. Para naman hindi ka lumobo pagkatapos ng quarantine period, magandang simulan ang iyong araw sa exercise. Walang gym? Don’t worry, mag-YouTube gym muna. Maraming fitness videos online na pwedeng mong sabayan. Marami ring fitness apps sa phone para naman magkaroon ng variation ang workout mo.

At dahil limited lang ang access mo sa fast food chain ngayon, now is the time to be healthy. You have all the time in the world to cook healthy and delicious meals. Na-enjoy mo na ang lutong-bahay, napalakas mo pa ang resistensya mo. Mas malaki ang chance na maiwasan ang virus by becoming fit and healthy every day.

DO GENERAL CLEANING

Dati parati kang nagre-reklamo na you do not have time to clean up. Sobrang busy. Pwes ngayon, wala kang choice kung hindi maglinis dahil buong araw kang nasa bahay. Sabi ni Pangulong Duterte, baka may mga lugar pa sa bahay natin na hindi pa natin napupuntahan. Baka naman din may lugar pa sa bahay natin na hindi pa napupuntahan ng walis. Kaya take advantage of this quarantine period. Baliktarin mo na ang iyong bahay and do general cleaning. Iwas bagot na, na-sanitize mo pa ang iyong tahanan.

LEARN AND RELEARN

Ito ang best part sa quarantine period. May time na tayong lahat para aralin ang mga bagay na hindi natin akalaing maaaral pa natin. Hindi na excuse ang walang time to learn and relearn. What is that thing that you really want to learn? Stock market? Music? Cooking? Makeup? Carpentry? Gardening? Sulitin natin ang quarantine period para matuto ng mga bagong skills o matuto muli ng mga nakalimutang skills. Huwag ding kalimutang magbasa-basa kahit isang oras kada araw. Marami kang matututunan sa pagbabasa kaysa ubusin mo ang buong araw sa pag-ubos sa catalogue ng Netflix at mga cat videos sa YouTube.

Importante sa panahon ngayon na magkaroon tayo ng daily routine para mayroon tayong sense of organization and for our sanity na rin. Si Earl na early bird ay sinisimulan niya ang kanyang araw nang maaga para mag-exercise at magluto ng healthy meals. ‘Di lang early bird si Earl. Masipag pa siya dahil may oras siya araw-araw na magwalis-walis man lang. At sa siesta hours, imbes na tumulala ay nagbabasa siya ng mga libro pati na mga online books.

Sa panahon ngayon, tayo’y maging early bird at masipag. Be like Earl.

“Ito na ang panahon upang magsipag at hindi magsayang ng oras. Huwag tayong maging Juan Tamad na nag-aantay lang na bumagsak ang prutas.” Chinkee Tan, Filipino Motivational Speaker

THINK. REFLECT. APPLY.

Anong pinagkakaabalahan mo ngayong quarantine?

May daily routine ka ba?

Anu-ano ang mga nais mong aralin ngayon na marami ka ng oras?

For more inspirational content, new products, and promos, follow my Social Media accounts:

Are you planning to invest in Pagibig MP2 savings? This guide will explain everything you need to know before getting started. There’s so much volatility when investing. That’s why finding a stable and rewarding savings platform is a treasure.

The Pag-IBIG MP2 Savings program offers Filipinos a unique, government-backed investment opportunity that promises impressive returns and supports nation-building. This guide provides a comprehensive overview of the Pag-IBIG MP2 Savings program, its advantages, and how one can start investing in it.

What is Pagibig MP2 Savings?

The Home Development Mutual Fund (HDMF), more commonly known as Pag-IBIG (short for Pagtutulungan sa Kinabukasan: Ikaw, Bangko, Industria at Gobyerno), was established to provide Filipinos with a nationwide savings system and affordable housing financing.

Watch this video to learn more about Pagibig MP2 fund:

The Pagibig MP2, or Modified Pag-IBIG II, is a voluntary savings scheme launched by the Pag-IBIG Fund to supplement its regular savings program. It’s designed specifically for members who wish to save more and earn higher dividends than the regular Pag-IBIG savings program.

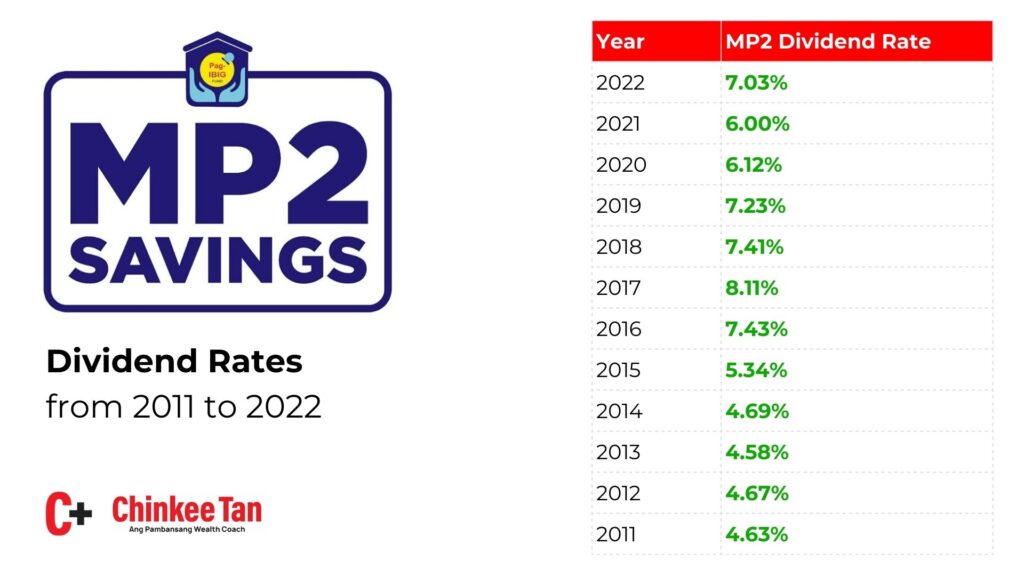

Check out the savings rate performance from the past few years:

Key Features and Benefits of Pagibing MP2 Savings

These are some key features and benefits of Pagibig MP2 savings to help you understand it better:

High Dividend Rates: Unlike traditional savings or time deposits in banks, MP2 dividends are derived from the Fund’s annual net income, making it potentially higher. The actual rate can vary yearly, but it has historically outperformed many commercial bank rates.

Tax-Free Dividends: The earnings from MP2 Savings are tax-exempt, ensuring that members benefit from their savings.

Guaranteed by the Government: MP2 Savings is backed by the Philippine government, ensuring the safety and security of members’ savings.

Flexible Contribution: While the regular Pag-IBIG savings program has a fixed monthly contribution, MP2 offers flexibility. Members can decide on their monthly contributions, allowing them to invest based on their financial capability.

Short Maturity Period: MP2 has a maturity period of 5 years, after which members can choose to withdraw their savings or let it roll for another five years, continuously earning dividends.

Why Should I Invest in MP2?

So why should you invest in Pagibig MP2? When deciding where to park your hard-earned money, there are several factors to consider: return on investment, safety, flexibility, and ease of transaction.

The MP2 Savings program ticks all these boxes. These make it a compelling choice for seasoned investors and those starting their savings journey. Let’s discuss these advantages:

1) Competitive Dividend Rates

In an era where traditional bank savings accounts offer meager interest rates, the MP2 program frequently boasts annual dividend rates that surpass these conventional savings mechanisms. This means your money works harder without you taking on excessive risks.

2) Security and Peace of Mind

Being a government-backed program, the MP2 Savings program is virtually risk-free. While no investment is 100% without risk, the backing of the Philippine government provides members an additional layer of assurance.

3) Flexibility for All

Whether you’re a high-income earner or someone with a tight budget, MP2’s flexibility in terms of contribution allows for a tailor-made savings plan. You decide how much you want to save monthly, ensuring you don’t overextend your finances.

4) Tax-Free Growth

Taxation can eat into your savings or investment growth. But with MP2’s tax-free dividends, you’re assured that every peso you earn as a dividend goes straight to your pocket, maximizing your overall returns.

Do You Want to Grow Your Wealth and Experience Financial Success?

Here, I’ll teach you all you need to know to grow authentic wealth while building a life filled with joy and contentment. You’ll also learn tips and strategies to grow your income no matter your industry. This training is perfect for employees, aspiring entrepreneurs, existing business owners, and OFWs.

And like I said, this training is absolutely free! So don’t miss this chance. Slots are limited, so sign up now by clicking on the button above or the link below.

Starting your investment journey with Pag-IBIG MP2 is a straightforward process. Depending on your preference, you can choose to enroll online or go through the manual enrollment procedure. Below are step-by-step guides to both processes:

Enter your Pag-IBIG Membership ID (MID) number and other required personal details.

Input the “CAPTCHA code” displayed on the screen and click “Submit” to proceed.

In the “Desired Monthly Contribution” field, indicate the amount you wish to contribute each month.

Based on your financial strategy and needs, select from the following options:

Dividend payout: Decide how you’d like to receive your dividends.

Payment mode: Choose your payment method, whether through salary deduction, over-the-counter, or other available modes.

Source of funds: Indicate the origin of your investment, be it from personal savings, salary, or other sources.

Click “Submit” to complete the online registration process.

A form displaying your 12-digit MP2 savings account number will appear upon successful enrollment. It’s essential to save this document as a PDF or print it for your records and future reference.

Pag-IBIG MP2 Manual Enrollment Procedure

Locate and visit the nearest Pag-IBIG branch to your location.

Approach a Pag-IBIG officer to request an MP2 Enrollment Form. Alternatively, you can download the form from the official Pag-IBIG website before your visit.

Carefully input all required information on the MP2 Enrollment Form, including your Pag-IBIG MID number.

Specify the amount you plan to contribute each month in the designated field.

Specify Your Preferences: Choose your desired options concerning the following:

Dividend payout: Select how you wish to receive your dividends.

Payment mode: Indicate your preferred payment method.

Along with the completed enrollment form, provide the necessary Pag-IBIG MP2 requirements:

A photocopy of a valid government-issued ID (like a passport or driver’s license).

Proof of income, which could be in the form of a payslip, certificate of employment, or any relevant document.

Make the first contribution as instructed by the Pag-IBIG officer assisting you.

Retain a copy of the filled MP2 Enrollment Form and the receipt as evidence of your successful enrollment.

Pag-IBIG MP2 Payment Options

Navigating through the modes of payment for the Pag-IBIG MP2 can be a breeze if you’re familiar with the available options. From traditional salary deductions to tech-savvy online channels, there’s a convenient method for everyone.

Salary Deduction

If you’re currently employed and your employer actively participates in the Pag-IBIG MP2 Salary Deduction Program, this mode can be seamless. Your monthly contributions are automatically deducted from your salary, ensuring timely payments without the hassle.

Over-the-Counter Payment

For those who prefer making transactions in person, you can easily walk into any Pag-IBIG branch or their accredited payment centers. Whether you’re paying in cash or using a check, the staff will guide you through the process, ensuring your payment is accredited to your MP2 account.

Online Payment Channels

If you’re tech-savvy or appreciate the convenience of online transactions, there are many platforms at your fingertips:

GCash: A popular e-wallet in the Philippines, GCash allows for quick and easy MP2 payments.

Coins.ph: Another favored digital wallet that facilitates Pag-IBIG transactions.

Moneygment: This app not only enables MP2 payments but also provides a range of financial management tools.

Other Online Facilities: Various online payment services partner with Pag-IBIG, expanding your range of choices.

Credit Card Options: Whether you have a Maya, Visa, Mastercard, or JCB credit card, you can utilize them for your MP2 contributions.

Online Banking

Many banks in the Philippines have integrated Pag-IBIG MP2 payment services into their online banking platforms. It’s worth checking with your bank to see if this facility is available, offering you an additional avenue to manage your contributions. You can check if your bank will allow online banking transfers for Pagibig MP2 here.

Frequently Asked Questions (FAQs)

Who is eligible to invest in Pagibig MP2?

Understanding eligibility is the first step to unlocking the potential of the Pag-IBIG MP2 Savings Program.

Current Pag-IBIG Fund Members

If you’re already a member of the Pag-IBIG Fund, the door to the MP2 Savings Program is wide open. This includes:

Local and Overseas Workers: Regardless of your location, if you’re an active Pag-IBIG member, you’re eligible.

Membership Types: Whether you’re a voluntary contributor, under mandatory employment coverage, or a self-employed individual, MP2 is within your reach.

New Contributors

Haven’t joined the Pag-IBIG Fund family yet? No worries! Prospective members can enroll in the regular Pag-IBIG program and subsequently apply for the MP2 Savings Program, making the scheme accessible even for newcomers.

How much is the MP2 monthly contribution?

The beauty of the MP2 Savings Program is its flexibility. There isn’t a fixed monthly amount; however, the minimum contribution is typically set by Pag-IBIG. Participants of the Pag-IBIG MP2 savings program must contribute at least PHP 500 monthly from their earnings, but they can increase their contribution up to PHP 25,000 monthly based on their income.

How much do I need to invest in Pag-IBIG MP2?

The initial investment or contribution depends on your financial capability and goals. While there is a set minimum amount, there’s no maximum limit, allowing you to invest as much as you’re comfortable with.

Can I withdraw my MP2 savings before 5 years?

The MP2 is a five-year term savings program. Early withdrawal is possible but might come with certain conditions. Some of those conditions include:

Total disability or insanity

Separation from service due to health reasons

Death of the member or immediate family member

Retirement (except for when the MP2 Saver is already a retiree)

Permanent departure from the country

Distressed member due to unemployment (layoff or company closure)

Critical illness of the member or immediate family member, certified by a licensed physician and approved by Pag-IBIG Fund

Repatriation of an Overseas Filipino Worker member

Other approved meritorious grounds by Pag-IBIG Fund

Can I pay for MP2 in one lump sum?

Absolutely! If you have the means and prefer to make a one-time payment rather than monthly contributions, you can opt for a lump sum payment. This can be especially advantageous if you’re considering the compounding effect of dividends over the 5-year term.

Final Words

Investing in the Pag-IBIG MP2 Savings Program offers Filipinos a fantastic avenue to grow their savings securely and hassle-free. Whether you’re an existing member of the Pag-IBIG Fund or someone looking to dip their toes into the world of savings and investments, MP2 provides a flexible, accommodating platform.

The MP2 program stands out as a top choice for those wanting to take control of their financial future. As always, research and consult with Pag-IBIG’s official channels and make informed decisions that resonate with your financial aspirations. Your future self will undoubtedly thank you for your prudent steps today!

Are you seeking a financial instrument to protect you from life’s uncertainties and help grow your wealth? You should consider getting life insurance. In this article, I’ll discuss life insurance benefits and how to get one in the Philippines.

If you’ve built up your income and savings and taken care of any outstanding debts, you’re ready to protect your wealth through insurance. Read on to learn why you should get life insurance when to get one, how to get one, and more.

What Is Life Insurance?

Life insurance is a crucial financial tool that provides protection and peace of mind for you and your loved ones. It offers a safety net for breadwinners against the uncertainties of life and ensures that your family is financially secure even in your absence.

You can also think of life insurance as a contract between you and the insurance company. You pay regular premiums in exchange for a payout to your beneficiaries upon your passing. This payout, known as the death benefit, can take care of your family’s financial needs and well-being after you’re gone.

Life insurance has become more popular over time. In 2017, there were only 7.88 million newly insured Filipinos. But in 2020, that number jumped to 24.9 million. But there are still many people who don’t have life insurance yet. You might be one of them. If you are, don’t worry! It’s not too late.

Nowadays, it’s not enough just to be a wise saver. Even if you save a million pesos today, that amount could be worth way less than ten to fifty years from now. Also, emergencies like sickness, business failure, and other financial catastrophes can easily wipe out savings. That’s why you need life insurance.

The Top 10 Benefits of Life Insurance Explained

Protecting the financial well-being of your loved ones should be a priority. Would you agree? We should be wise to protect ourselves from surprises like the main earner losing their income. The best way to do that is to cover yourself with life insurance to provide that security.

Here are the ten key benefits life insurance brings. Read on to understand how this vital financial tool can safeguard your family’s future.

1) Security for Your Loved Ones

Life insurance serves as a safety net, assuring that your family remains financially protected, maintaining their quality of life even in your absence. This is highly recommended especially if you are the breadwinner of the household.

2) Coverage for Immediate Costs

A life insurance policy covers more than just the distant future. It also takes care of immediate expenses like hospitalization, funeral, and burial costs, easing the financial burden on your family during an already challenging time.

3) Debt Settlement

Outstanding debts like loans and mortgages need not concern your family. The insurance payout can be utilized to settle these financial obligations, providing relief and security. By eliminating the liability early on, your family can focus on rebuilding your lives, making important decisions, and planning for the future without the shadow of debt hanging over them.

In essence, a well-thought-out life insurance policy can protect the family from potential financial strains and offer them the peace of mind they deserve.

4) Savings and Investments

Some life insurance policies, such as permanent life or VUL, offer a dual advantage. Over time, they build up cash value, serving as protection and an accessible savings resource when needed.

5) Replacing Lost Income

The death benefit from a life insurance policy can serve as a crucial income replacement, ensuring that your family can continue to meet daily expenses without unnecessary stress. Some life insurance also have critical illness coverage that will help with your expenses if you experience debilitating illnesses.

6) Education Fund Assurance

Securing your children’s education is a priority for every parent. As tuition fees and educational expenses rise, ensuring your children can continue their studies without financial stress becomes even more critical.

Life insurance plays a crucial role in this regard. It acts as a financial safety net, ensuring that your children’s education fund remains untouched, despite unforeseen events that may befall the family.

7) Safeguarding Businesses

For those who play a pivotal role in a business, their sudden absence can have far-reaching consequences. Life insurance becomes an essential tool in such scenarios. It safeguards the company from potential financial setbacks and disruptions that might arise from the sudden loss of a key person.

With the right policy in place, businesses can maintain their operations, settle debts, and ensure that employees’ livelihoods are not affected. Entrepreneurs and business leaders can ensure the continued stability and prosperity of the company they’ve worked hard to build.

8) Relief from Financial Burdens

Life can be unpredictable, and financial burdens accumulate over time, from mortgages to loans and other liabilities. A well-structured life insurance policy can be a financial pillar during such challenging times.

It can act as a lifeline, settling significant debts such as home, car, or even personal loans. Additionally, in many jurisdictions, life insurance can be a tool to address transfer or inheritance taxes, ensuring that beneficiaries receive their due without added financial strain.

9) Tailored Additional Riders

Life insurance isn’t a one-size-fits-all solution. The beauty of modern insurance policies is their adaptability. Policyholders can enhance their coverage with tailor-made riders that cater to specific needs.

These additional riders can be integrated into the primary policy for protection against accidents, critical illnesses, or disability.

10) Peace of Mind

Ultimately, life insurance’s most significant benefit is its peace of mind. Knowing that your loved ones are financially safeguarded allows you to enjoy life fully, secure in knowing that your family’s future is protected.

This protection ensures that the family’s future remains secure even in the face of adversity. With this peace of mind, individuals can embrace life’s adventures, cherish moments, and build lasting memories, knowing that their family’s well-being is always prioritized.

Do You Need More Guidance?

Insurance is but one part of the whole wealth-building equation. If you’d like to get on track to start your journey toward financial freedom, I’d like to invite you to join our community called “The Yayamanin Life.”

Here, you will learn all the best strategies and principles to protect your income, grow your wealth, and experience financial prosperity. This community includes all kinds of financial training and programs, including:

A monthly coaching session with me, Chinkee Tan, a wealth coach who has helped thousands of people become wealthy and debt-free.

A library of courses to teach you how to create, handle, invest, and protect your wealth.

Accountability groups to fast-track your progress.

Daily tips and financial insights.

And more!

We’re also running a limited promo where you can get up to 50% off if you pay for one year in advance. To join this program, click here now.

Choosing the right life insurance policy is one of your most significant financial decisions. It’s a step toward ensuring the well-being of your loved ones even when you’re not around. This process may seem complex, but breaking it down into manageable steps can help you confidently navigate the options.

Here’s a comprehensive roadmap to make an informed decision about your life insurance coverage.

1) Determine Your Needs

The first step in choosing the right life insurance policy is understanding your family’s financial needs. Consider your current financial obligations – mortgage, loans, and debts – and consider future expenses like your children’s education costs.

It is essential to estimate the income your dependents would need to maintain their lifestyle in your absence. This information will be the foundation for selecting an appropriate coverage amount.

2) Assess Your Current Financial Situation

Before you dive into the world of life insurance, evaluate your existing financial portfolio. This includes your assets, savings, investments, and any other insurance policies you might have. Having a clear picture of your financial health will help you understand where life insurance fits into your overall plan.

3) Set Clear Objectives

Consider your long-term objectives. Are you seeking temporary coverage to protect your family during a specific period, or do you want lifelong protection with potential financial benefits?

Your choice will guide you toward term insurance, which covers you for a set period, or permanent insurance, such as whole life or universal life, which provides coverage for your entire life and may have a cash value component.

4) Understand the Types of Insurance

Before making an informed decision, you need to understand the types of life insurance available. Later in this article, I’ll discuss the different types of insurance and their pros and cons, so keep reading.

5) Calculate the Coverage Amount

Determining how much coverage you need requires careful consideration. Online calculators can help you estimate the right coverage amount based on your financial situation, obligations, and the needs of your beneficiaries. Consulting with a financial professional can provide valuable insights if you’re unsure.

6) Research Insurance Companies

Not all insurance companies are created equal. Research the financial strength of potential insurers. Look into their reputation for customer service and their claim settlement ratios. A strong, reliable insurance company is crucial for ensuring your beneficiaries receive the promised benefits when the time comes.

Check out this list of the most popular insurance companies in the Philippines:

Part of the AXA Group, a worldwide leader in insurance and asset management. AXA Philippines started operations in 1999 and has since been a major player in the country.

Renowned for its integrated financial services, strong digital initiatives, and comprehensive product range.

7) Compare Premiums

Affordability is key, but remember that the cheapest premium might not offer the best coverage. Balancing costs with benefits is essential. Look for a policy that offers reasonable premiums while providing the coverage your family needs.

8) Consult a Financial Advisor or Insurance Agent

When in doubt, seek guidance from experts in the field. Financial advisors and insurance agents can provide personalized advice tailored to your situation. They can explain complex terms, answer your questions, and ensure you’re making an informed choice.

The Different Kinds of Life Insurance

Before you decide to get life insurance, you must know that several types of life insurance policies are available in the Philippines, each designed to cater to specific needs. Understanding these options will help you decide the type of coverage that suits you best.

1) Term Life Insurance

Term life insurance is similar to car insurance and provides annual coverage, typically you renew this on an annual basis. If you pass away during the policy term, your beneficiaries receive the death benefit.

Pros

Affordability: Term life insurance is generally more affordable than permanent life insurance options, making it an attractive choice for individuals on a budget.

Simplicity: The straightforward structure of term life insurance makes it easy to understand. You pay a fixed premium for a specific term; if you pass away during that term, your beneficiaries receive the death benefit.

Flexible Coverage: You can choose the policy term that aligns with your specific needs. This is particularly useful when you have short-term financial responsibilities such as paying off a mortgage or funding your children’s education.

Cons

Limited Duration: Term life insurance only covers a specified period. If you outlive the policy term, you won’t receive any benefits, and the coverage ends.

No Cash Value: Unlike permanent life insurance policies, term life insurance does not accumulate a cash value over time. This means you can’t borrow or withdraw funds from the policy.

2) Traditional or Permanent Life Insurance

Traditional or Permanent life insurance offers coverage for your entire life as long as you continue to pay the premiums.

Pros

Lifelong Coverage: This provides peace of mind knowing that your beneficiaries will receive the death benefit regardless of when you pass away.

Cash Value Accumulation: One of the most significant advantages of permanent life insurance is accumulating cash value over time. This cash value can be used for various purposes, such as supplementing retirement income, paying off loans, or covering emergencies.

Tax Benefits: The cash value growth in a permanent life insurance policy is tax-deferred, meaning you don’t pay taxes on the growth until you withdraw the funds.

Cons

Higher Premiums: Permanent life insurance policies typically have higher premiums than term life insurance. This can be a drawback for individuals looking for more affordable coverage.

Complexity: Due to the cash value component, Permanent life insurance policies can be more complex than term policies. Understanding the policy’s features and potential returns requires careful consideration.

3) Variable Universal Life (VUL) Insurance

Variable Universal Life (VUL) insurance is a type of permanent life insurance that combines elements of traditional life insurance with investment options.

Pros

Investment Opportunities: VUL policies allow policyholders to invest a portion of their premiums in various investment funds, potentially leading to higher returns over time.

Flexibility: VUL offers flexibility in terms of premium payments and death benefits. You can adjust the amount of coverage and investment allocations as your financial situation changes.

Cash Value Growth: Similar to other permanent life insurance, VUL policies accumulate cash value over time, which can be used for various financial needs.

Cons

Market Risk: The investment component of VUL policies is not guaranteed and exposes the policyholder to market fluctuations and risks. Poor investment performance could negatively impact the policy’s cash value and death benefit.

Higher Costs: VUL policies often come with higher fees and charges compared to traditional or permanent insurance due to the investment component. These costs can eat into potential returns and affect the overall policy value.

Complexity: Just like other permanent policies, VUL can be complex to understand due to the dual nature of insurance and investment. This complexity requires careful consideration and potentially the help of financial professionals.

Before deciding, it’s important to weigh the pros and cons of each type of insurance and consider your individual financial goals and circumstances. Consulting with a financial advisor or insurance professional can provide valuable insights to help you make an informed choice that aligns with your needs and objectives.

Frequently Asked Questions (FAQs)

What are the best life insurance companies in the Philippines?

Research and customer reviews are valuable resources for identifying reputable insurance providers in the Philippines. You should check and decide for yourself. But I highly recommend that you go with any of the companies above.

What is variable universal life insurance?

Variable Universal Life (VUL) insurance is a versatile option that combines life insurance coverage with investment opportunities. Policyholders can allocate their premiums to various investment funds.

What is permanent life insurance?

Permanent life insurance offers coverage for your entire life, often including a cash value component that grows over time.

Can you cash out life insurance before death?

Depending on your policy type, you might be able to surrender or withdraw funds from your life insurance while you’re alive. Keep in mind that this action could affect your coverage and cash value.

Final Words

Choosing the right life insurance policy is a decision that involves thoughtful consideration. It’s about securing your family’s financial well-being and protecting them, even if the unexpected occurs. By carefully following these steps, understanding the different types of insurance, and seeking expert advice when needed, you’re taking a significant step toward creating a stable future for your loved ones.

The benefits of any life insurance extend beyond your lifetime, providing enduring financial security and peace of mind. Your choice today becomes a legacy of protection and support your family can rely on for generations.

Everyone, if not most people, want to have financial security and prosperity. Yet, learning how to be rich isn’t only about monetary abundance; it’s about having a balanced life, emotional well-being, spiritual growth, and the freedom to pursue your passions in life.

This comprehensive guide is designed to provide Filipinos gain expert insights on wealth building and financial literacy. Being in the finance industry for over a decade, I want to help you lay that foundation to build wealthy and passive income in the Philippines.

How the Rich Live Their Lives: A Deeper Dive into True Wealth

When most people hear the word “rich”, they instinctively think of sprawling mansions, luxury cars, and opulent lifestyles. While it’s undeniable that financial abundance can afford such luxuries, the truly rich, in essence, lead lives that are grounded in principles far beyond material acquisitions. Here’s a closer look.

1. Prioritizing Growth and Learning Over Lifestyle Inflation

The wealthy have a unique mindset: they prioritize self-improvement and lifelong learning. This is not just about accumulating degrees or attending courses, but it’s an innate thirst for knowledge and personal development. They understand that their most significant asset isn’t their bank account but their mind and the breadth of experiences they gather throughout their life.

In stark contrast to this growth-centric approach is the trap of lifestyle inflation. As income increases, it’s all too tempting to elevate one’s lifestyle at the same pace. While there’s a joy in indulging and celebrating financial successes, it becomes problematic when every raise or bonus leads to increased expenditures, leaving little room for meaningful investments and personal growth. The truly rich ensure that while their wealth grows, it doesn’t come at the expense of their learning or personal development.

2. True Riches Beyond Monetary Measure

Being rich isn’t just about the numbers in a bank statement. It’s a holistic wealth encompassing emotional, spiritual, and physical dimensions. Here’s how the genuinely rich view these dimensions:

Emotional Wealth: Richness in life is also about having deep, meaningful relationships and emotional stability. The emotionally wealthy can navigate life’s ups and downs with resilience, draw strength from their relationships, and find joy in small, everyday moments.

Spiritual Wealth: Whether it’s adhering to a particular faith or finding solace in personal beliefs or practices, spiritual wealth offers a sense of purpose. It provides the truly rich with a compass to navigate life’s challenges, find meaning in adversity, and remain anchored amidst external chaos.

Physical Wealth: Health is often said to be true wealth. Without health, even the most abundant financial wealth loses its sheen. The genuinely rich understand this and prioritize their health, investing time and resources into maintaining their well-being, and pursuing activities that nourish their physical selves.

3. The Luxury of Time Freedom

A coveted aspect of true richness is having control over one’s time. Financial abundance can provide the means to pursue passions, spend moments with loved ones, or even take breaks to rejuvenate and reflect. The genuinely rich value time as their most precious resource and strive for a life where they can allocate it as they see fit, without being shackled by endless obligations.

Rich vs Poor Mindset: How the Wealthy Think

Understanding the intricacies of wealth isn’t just about counting dollars and cents; it’s about the mindset that paves the way to financial abundance. The way we think, perceive opportunities, and react to challenges can significantly shape our financial journey.

Here’s a comparison of the mindset between those who often find wealth and those who might struggle, regardless of their current financial status.

1. Long-term vs Short-term Vision

Rich Mindset: Long-term Vision— Those with a wealthy mindset are frequently future-oriented. They set long-term goals, understanding that true wealth and success don’t happen overnight. Their decisions are made based on how it will benefit them in the long run, rather than immediate gratification. Whether it’s about investments, career moves, or personal growth, they’re in it for the long haul.

Poor Mindset: Short-term Vision— In contrast, a short-term perspective might focus more on immediate rewards and gratifications. This might lead to impulsive decisions without considering the long-term implications. It’s the allure of instant pleasure over future benefits.

2. Embracing vs Avoiding Risk

Rich Mindset: Embracing Risk— Wealth often comes with taking calculated risks. The wealthy mindset understands that without stepping out of one’s comfort zone, significant rewards might remain elusive. They evaluate risks, prepare for them, and see failures as learning experiences rather than setbacks.

Poor Mindset: Avoiding Risk— Over-caution will often cause missed opportunities. While it’s essential to be wary of potential pitfalls, avoiding all risks can result in stagnation. A mindset dominated by fear might miss out on potentially lucrative chances.

3. Saving vs Investing

Rich Mindset: Investing— While saving is essential, the wealthy know that the real growth of their money comes from smart investments. They educate themselves on the best opportunities, whether in stocks, real estate, or businesses, and understand the power of compounding and how it can amplify their wealth over time.

Poor Mindset: Saving— Simply stashing money away might give a sense of security, but inflation and changing economic climates can erode its value over time. Relying solely on savings without considering investments might lead to missed wealth-building opportunities.

4. Improving Lifestyle vs Income

Rich Mindset: Improving Income — Instead of just elevating their lifestyle with each financial increase, those with a wealthy mindset focus on increasing their income streams. They look for new opportunities, ventures, and ways to diversify their income. The goal is sustainable and scalable wealth.

Poor Mindset: Improving Lifestyle — Immediate elevation of lifestyle with every small financial gain can lead to a cycle of living paycheck to paycheck. While it’s essential to enjoy life, doing so without ensuring a steady and increasing income can lead to potential financial pitfalls.

Ten Key Principles for Building Sustainable Wealth

1) Set Clear Financial Goals

Effective wealth building begins with setting clear, well-defined financial goals. These goals serve as your roadmap, providing direction, motivation, and a sense of purpose in your journey toward financial prosperity.

Reflection Question: Have you defined specific financial goals that guide your actions and decisions?

2) Manage Your Expenses

One of the cornerstones of wealth building is strategic expense management. Minimizing wasteful spending frees up resources for wealth accumulation. Every peso saved brings you a step closer to the ultimate goal of financial freedom.

Reflection Question: Have you defined specific financial goals that guide your actions and decisions?

3) Learn How to Consistently Save

Setting aside a significant portion of your income regularly establishes a solid foundation for your financial future. This consistent effort lays the groundwork for achieving your financial aspirations.

Reflection Question: Do you regularly set aside a portion of your income?

4) Pay off Your Debts

The burden of debt can impede your journey toward wealth. Prioritizing debt elimination through systematic and informed strategies liberates resources that can be redirected toward wealth-building endeavors.

Reflection Question: How might focusing your resources to debt payments accelerate your progress?

5) Build Your Emergency Fund

Life is full of unexpected twists and turns. An emergency fund acts as a safety net, providing financial security during unforeseen challenges. It ensures that you’re well-equipped to weather storms without derailing your overall financial progress.

Reflection Question: Have you prioritized and set up an emergency fund that can provide you with peace of mind during unexpected challenges?

6) Start Investing As Early as Possible

Time is a powerful ally when it comes to wealth building. Initiating early investments allows you to harness the compounding effect, which amplifies your returns over the long term. This means that even small investments made early can yield substantial outcomes.

Reflection Question: Have you started on any early investments to build on your long-term wealth?

7) Diversifying for Risk Management

A critical principle in wealth building is diversification. Spreading your investments across various asset classes helps mitigate risks associated with market volatility. Diversification optimizes potential returns while minimizing the impact of any single investment’s underperformance.

Reflection Question: How might diversification help you mitigate the risks associated with market volatility?

8) Create Multiple Income Streams

Relying solely on a single income source can limit your financial growth potential. By creating and nurturing multiple income streams, you insulate yourself against economic downturns and create a stable foundation for wealth accumulation.

Reflection Question: Do you have multiple income streams set aside from your current income?

9) Invest in Financial Education

Empowerment through knowledge is a key aspect of wealth building. Investing time and effort in financial education equips you with the insights and understanding needed to make informed investment decisions and manage your finances more effectively.

Reflection Question: What role does ongoing financial education play in making informed investment decisions?

10) Avoid Get Rich Quick Schemes

I believe that everyone should build wealth on a foundation of patience, strategy, and disciplined effort. Get-rich-quick schemes may promise instant riches, but they often lead to disappointment and financial setbacks. Avoiding such shortcuts is crucial to your long-term financial success.

Reflection Question: Have you lost some money in investing in wrong business and investment opportunities?

Crunching the Numbers: A Savings and Investment Blueprint

Maybe you’re thinking: “Can I really become financially rich?” You’ll be surprised how your wealth can grow with the right habits of saving and investing.

To illustrate the impact of disciplined savings and investments, consider two scenarios over a ten-year period:

Scenario 1: Saving and Investing 60,000 Pesos Annually

Scenario 2: Saving and Investing 72,000 Pesos Annually

These scenarios offer practical insights into the transformative potential of consistent contributions and compounding interest.

If you saved and invested 60,000 a year (or 5,000 a month).

Year

Savings at the Beginning of the Year

Interest Earned

Total Savings at the End of the Year

1

60,000

4,800

64,800

2

124,800

9,984

134,784

3

194,784

15,583.52

210,367.52

4

265,367.52

21,229.40

286,596.92

5

336,596.92

26,927.75

363,524.67

6

409,524.67

32,761.97

442,286.64

7

484,286.64

38,742.93

523,029.57

8

561,029.57

44,871.57

605,901.14

9

639,901.14

51,148.09

691,049.23

10

721,049.23

57,570.34

778,619.57

11

804,619.57

64,135.56

868,755.13

12

890,755.13

70,839.61

961,594.74

13

959,594.74

76,677.18

1,036,271.92

14

1,036,271.92

82,642.15

1,118,914.07

If you saved and invested 72,000 a year (or 6,000 a month).

Year

Savings at the Beginning of the Year

Interest Earned

Total Savings at the End of the Year

1

72,000

5,760

77,760

2

149,760

11,980.80

161,740

3

233,740

18,699.20

252,439.20

4

322,439.20

25,795.14

348,234.34

5

417,234.34

33,378.75

450,613.09

6

517,613.09

41,409.05

559,022.14

7

623,022.14

49,841.77

672,863.91

8

732,863.91

58,629.11

791,493.02

9

847,493.02

67,730.64

915,223.66

10

967,223.66

77,102.69

1,044,326.35

The CHIP Method: Your Comprehensive Wealth Management Strategy

The road to financial success isn’t solely about amassing money; it’s about how you manage, grow, and protect that wealth. This is where I want to introduce you to the CHIP method, a framework that provides a comprehensive plan that helps you experience financial success and escape financial stress.

Let me explain this framework to you:

1. Creating Wealth

Foundational Principle: Before managing wealth, one must create it.

Generating Income: The first step is to have a stable source of income, whether it’s from employment, a business, freelance work, or other entrepreneurial ventures. Exploring multiple income streams can accelerate wealth creation.

Saving Prudently: It’s not about how much you earn, but how much you save. Prioritizing savings, even when the income is modest, can accumulate significant wealth over time. Following the age-old advice of “paying yourself first” ensures that a portion of every earning is set aside for the future.

2. Handling Wealth

Foundational Principle: Effective money management ensures that wealth grows rather than stagnates.

Budgeting: Crafting a well-defined budget and adhering to it helps allocate resources efficiently. It ensures that expenses don’t overrun income, and savings goals are consistently met.

Responsible Spending: Adopting a frugal mindset doesn’t mean depriving oneself. It’s about discerning between needs and wants and making purchases that offer long-term value.

Avoiding Lifestyle Inflation: As income grows, there’s a temptation to upscale the lifestyle proportionately. While it’s natural to want to enjoy increased earnings, unchecked lifestyle inflation can quickly erode new wealth.

3. Investing Wealth

Foundational Principle: Money should work for you, not the other way around.

Educate Before You Invest: Jumping blindly into investments is risky. Before channeling resources, one should understand the venture, its risks, and potential returns.

Diversification: Not putting all eggs in one basket reduces risk. Spreading investments across different assets—stocks, bonds, real estate—ensures that if one underperforms, others might compensate.

Aligned Financial Goals: Investments should reflect one’s financial objectives, whether it’s early retirement, buying a home, or building a college fund for children.

4. Protecting Wealth

Foundational Principle: Wealth preservation is as crucial as its creation.

Insurance: From life to health and property insurance, having the right protection ensures that unforeseen events don’t decimate hard-earned wealth.

Estate Planning: Effective estate planning ensures that one’s assets benefit their loved ones in the event of their passing, rather than being caught up in legal complexities.

Risk Management: Beyond insurance, this involves understanding the financial risks in one’s life and taking steps to mitigate them. This could mean diversifying investments, setting up emergency funds, or avoiding high-interest debt.

If you want me to coach you on the CHIP method, I want to invite you to be a part of The Yayamanin Life Coaching program. This online coaching group is an exclusive club of Filipinos dedicated to becoming financially wealthy and debt-free.

When you join this program, you will get access to:

Dozens of high-value trainings and courses from me and many other financial experts and coaches in the Philippines. Some include:

Marvin Germo

Bo Sanchez

Maj Custodio

Randell Tiongson

Carlo Ople

And so many more!

A monthly coaching session with me— Wealth Coach Chinkee Tan. Together, we’ll unpack lessons and practices that help you become truly wealthy.

Accountability groups to help you reach your financial goals.

Ask me anything groups so you can get more insights, learnings, and clarity.

An online community ready to keep you accountable and collaborate.

Is wealth-building feasible on a modest Philippine income?

Absolutely. With discipline and strategic planning, even a modest income can lead to substantial wealth accumulation over time. But you can reach your financial goals faster if you also learn how to grow your income. That’s why I believe you should create more wealth.

What secure investment opportunities exist in the Philippine market?

The Philippine stock market, real estate, and mutual funds offer viable options. Thorough research or professional advice is crucial before investing.

How can I initiate financial literacy with minimal prior knowledge?

Begin with freely available online resources, attend financial workshops, read reputable literature, and follow respected financial experts. Feel free to visit my YouTube channel to get more financial tips.

Can franchise businesses genuinely yield passive income?

While franchise businesses can provide passive income, success hinges on factors like location, brand reputation, and effective management.

How can I shield my wealth during economic downturns?

Diversify investments, maintain a robust emergency fund, and consider assets historically resilient during economic challenges.

Final Insights

Your journey of wealth building needs unwavering dedication, disciplined action, and an informed strategy. Through setting precise goals, managing expenditures wisely, making prudent investments, and adopting a prosperity-focused mindset, you can chart a course toward financial well-being.

Wealth goes beyond monetary gain; it empowers you to lead life on your own terms. Take the first step today and lay the foundation for a future marked by financial security and abundance.

Are you thinking of starting a small business in the Philippines? If you feel like you’ve ever run out of ideas, I’ve got you covered! There are so many ideas for small business owners and aspiring entrpreneurs.

If you’re looking for inspiration, we’ve compiled a list of 20 small business ideas you can consider. Whether you want to start a low-investment venture or a unique business, there’s something here for everyone.

Key Takeaways

Filipinos have all kinds of small business opportunities. I will only share a very small portion of the many other available ideas.

Starting a small business doesn’t always require a huge investment.

Unique business ideas can help you stand out in a competitive market.

The food and beverage, retail, and services industries are just a few examples of sectors with small business potential.

Exploring online business ideas can be a great way to reach a wider audience.

Explore Small Business Ideas in the Philippines

Ready to start your own small business in the Philippines? Look at our other sections to explore 20 small business ideas, online business ideas, unique small business ideas, small-scale business opportunities, low-investment business ideas, and small business ideas in different industries. Good luck!

Small Business Ideas for Beginners

Starting a business can be risky, especially if you’re new to entrepreneurship. Fortunately, plenty of small business ideas for beginners require little investment and can help you gain experience.

Here are some low-investment business ideas that you can consider:

Customized Gift Baskets: Tailored baskets filled with a curated selection of items catered to the recipient’s interests or occasion, making for a personalized and thoughtful gift.

Event Planning Services: Professional coordination and management of events, ranging from weddings to corporate functions, ensuring smooth execution and a memorable experience for attendees.

Cleaning Services: Offering thorough cleaning of homes, offices, or specific areas like carpets and windows, ensuring spaces remain hygienic and presentable.

Graphic Design Services: Artistic and technical services focused on creating visual content, including logos, marketing materials, and digital designs, to meet clients’ branding or promotional needs. You can get projects on Upwork or Fiverr.

Personal Shopping Services: Assisting clients in purchasing products based on their preferences, needs, or occasions, often combining knowledge of trends and personal styling expertise.

Home-based Baking: Crafting and selling baked goods, such as cookies, cakes, and pastries, from a home kitchen, often with options for customization.

Online Tutoring: Providing educational support and instruction in various subjects or skills via digital platforms, catering to students of different age groups and academic needs. There are also many other virtual professions you can apply for.

Pet Grooming Services: Tending to the hygiene and appearance needs of pets, including baths, haircuts, nail trimming, and other grooming essentials.

Handmade Crafts: Producing and selling unique, handcrafted items, such as jewelry, pottery, or textiles, often imbued with a personal touch and creativity.

Home-based Childcare Services: Offering safe and nurturing environments for children within a residential setting, often providing activities, meals, and supervision during specified hours.

These small business ideas for beginners don’t require prior experience and can be started with minimal investment. Dedication and hard work can turn any of these ideas into a profitable venture.

Online Business Ideas

The internet has opened up a whole world of opportunities, and starting an online business can be a great way to tap into that potential. In the Philippines, there are several online business ideas that you can explore. From e-commerce to digital marketing, here are the most promising ones:

Business Idea

Description

E-commerce store

One of the most popular online business ideas, e-commerce stores allow you to sell products or services online. With platforms like Lazada and Shopee, starting an online store has never been easier.

Digital marketing agency

If you have a knack for marketing, you can start a digital marketing agency that helps businesses promote their products and services online. This can include services like social media management, search engine optimization, and email marketing.

Content creation

Content is king, and there is a high demand for quality content creators online. You can start a business that creates content for other businesses or individuals, such as blog posts, articles, videos, and social media posts.

Online tutoring